What’s Going on with Home Prices? Ask a Professional.

What’s Going on with H

If you’re thinking about buying or selling a home this year, you may have questions about what’s happening with home prices today as the market cools. In the simplest sense, nationally, experts don’t expect prices to come crashing down, but the level of home price moderation will depend on factors like supply and demand in each local market.

That means, moving forward, home price appreciation will continue to vary by location, with more significant changes happening in overheated areas. Here’s a quick snapshot of what the experts are saying:

Danielle Hale, Chief Economist at realtor.com, says:

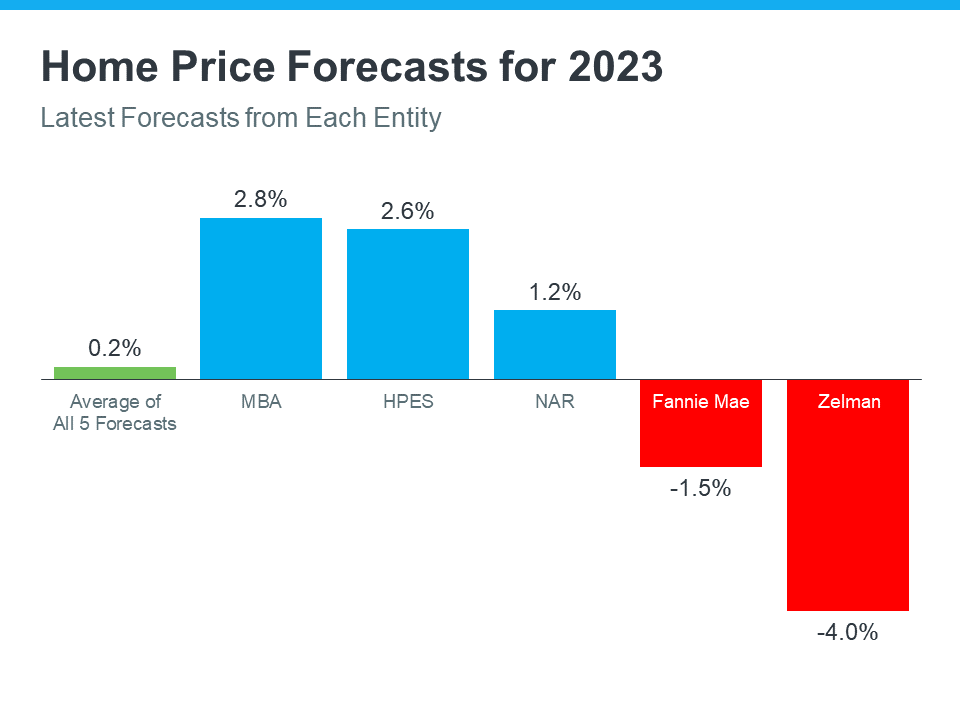

“The major question on the minds of homeowners and aspiring buyers alike is what will happen to home prices. . . Soaring prices were propelled by all-time low mortgage rates which are a thing of the past. As a result, home price growth is expected to continue slowing, dipping below its pre-pandemic average to 5.4% for 2023, as a whole.”

Mark Fleming, Chief Economist at First American, says:

“House price appreciation has slowed in all 50 markets we track, but the deceleration is generally more dramatic in areas that experienced the strongest peak appreciation rates.”

Taylor Marr, Deputy Chief Economist at Redfin, says:

“For those bearish folks eagerly awaiting the home price crash, you’ll have to keep waiting. As much as demand is pulling back supply is as well reducing downward pressure on prices in the short run.”

John Paulson, Founder of Paulson & Co., says:

“It’s true – housing may be a little frothy. So housing prices may come down or they may plateau . . .”

What Does This Mean for You?

The best way to get the answers you need is to lean on a local real estate advisor. They’ll be able to explain the latest trends in your specific market so you can make a confident and informed decision on your next step toward buying or selling a home.

Bottom Line

If you have questions about what’s happening with home prices today, let’s connect so you have the latest on our local market.