3 Key Factors Affecting Home Affordability

Over the past year, a lot of people have been talking about housing affordability and how tight it’s gotten. But just recently, there’s been a little bit of relief on that front. Mortgage rates have gone down since their most recent peak in October. But there’s more to being able to afford a home than just mortgage rates.

To really understand home affordability, you need to look at the combination of three important factors: mortgage rates, home prices, and wages. Let’s dive into the latest data on each one to see why affordability is improving.

1. Mortgage Rates

Mortgage rates have come down in recent months. And looking forward, most experts expect them to decline further over the course of the year. Jiayi Xu, an economist at Realtor.com, explains:

“While there could be some fluctuations in the path forward … the general expectation is that mortgage rates will continue to trend downward, as long as the economy continues to see progress on inflation.”

And even a small change in mortgage rates can have a big impact on your purchasing power, making it easier for you to afford the home you want by reducing your monthly mortgage payment.

2. Home Prices

The second important factor is home prices. After going up at a relatively normal pace last year, they’re expected to continue rising moderately in 2024. That’s because even with inventory projected to grow slightly this year, there still aren’t enough homes for sale for all the people who want to buy them. According to Lisa Sturtevant, Chief Economist at Bright MLS:

“More inventory will be generally offset by more buyers in the market. As a result, it is expected that, overall, the median home price in the U.S. will grow modestly . . .”

That’s great news for you because it means prices aren’t likely to skyrocket like they did during the pandemic. But it also means it’ll probably cost you more to wait. So, if you’re ready, willing, and able to buy, and you can find the right home, purchasing before more buyers enter the market and prices rise further might be in your best interest.

3. Wages

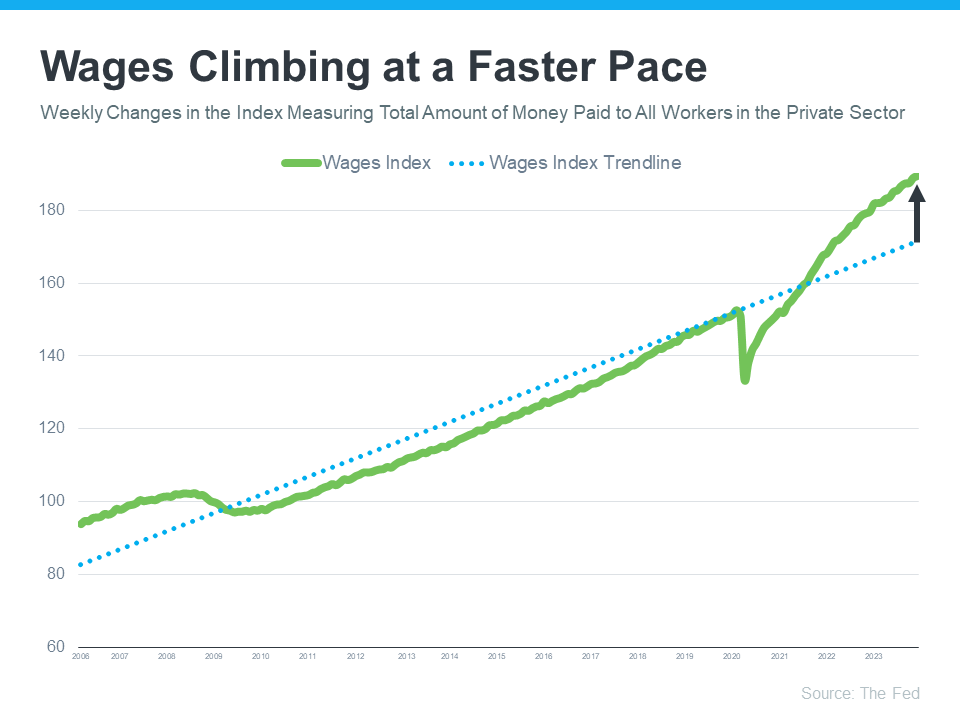

Another positive factor in affordability right now is rising income. The graph below uses data from the Federal Reserve to show how wages have grown over time:

If you look at the blue dotted trendline, you can see the rate at which wages typically rise. But on the right side of the graph, wages are above the trend line today, meaning they’re going up at a higher rate than normal.

Higher wages improve affordability because they reduce the percentage of your income it takes to pay your mortgage. That’s because you don’t have to put as much of your paycheck toward your monthly housing cost.

What This Means for You

Home affordability depends on three things: mortgage rates, home prices, and wages. The good news is, they’re moving in a positive direction for buyers overall.

Bottom Line

If you’re thinking about buying a home, it’s important to know the main factors impacting affordability are improving. To get the latest updates on each, let’s connect.

Homeownership Is Still at the Heart of the American Dream

Buying a home is a powerful decision, and it remains at the heart of the American Dream. Unlike renting, owning a home means more than just having a place to live – it offers a sense of belonging, stability, and freedom. According to Nicole Bachaud, Senior Economist at Zillow:

“The American Dream is still owning a home. There’s a lot of pent-up demand for ownership; that isn’t going to go away.”

Let’s explore just a few of the reasons why so many Americans continue to value homeownership.

The Financial Benefits of Owning a Home

One possible reason homeownership is viewed so highly is because owning a home is a significant wealth-building tool. That may be why Jessica Lautz, Deputy Chief and VP of Research at the National Association of Realtors (NAR), says:

“Homeownership is the number one way to build wealth in America.”

Over time, owning a home not only helps boost your own net worth, but it also sets future generations up for success as you pass that wealth down. Habitat for Humanity explains:

“Overall, homeownership promotes wealth building by acting as a forced savings mechanism and through home value appreciation. Homeowners make monthly payments that increase their equity in their homes by paying down the principal balance of their mortgage. . . . In addition, owning a home promotes intergenerational homeownership and wealth building. Children of homeowners transition to homeownership earlier — lengthening the period over which they can accumulate wealth . . .”

It can also provide meaningful financial stability compared to renting. When you buy with a fixed-rate mortgage, you can lock in your monthly housing payments for the length of your home loan.

The Non-Financial Benefits of Homeownership

But, owning a home offers more than just financial benefits—it benefits you socially and emotionally too. Your home provides feelings of achievement, responsibility, and more. In a recent survey, Fannie Mae outlines just a few of these more emotionally-driven benefits, including:

“The top three were having control over what you do with your living space (94%) to having a sense of privacy and security (91%) and having a good place for your family or to raise your children (90%) . . .”

What Does That Mean for You?

If your idea of the American Dream involves greater freedom, security, and prosperity, homeownership could be a key player in bringing that dream to life. And with mortgage rates now on a downward trend, it might be a good time for you to consider making a move.

If you’re ready and able to buy, know that there are incredible benefits waiting at the end of your journey. You’ll gain more than just a home – it’s a place to grow your wealth and call your very own. Like Ksenia Potapov, Economist at First American says:

“…homeownership remains an important driver of wealth accumulation and the largest source of total wealth among most households.”

Bottom Line

Buying a home is a powerful decision and the cornerstone of the American Dream. If finding a place to call your own is part of your dream for this year, let’s connect to start the process today.

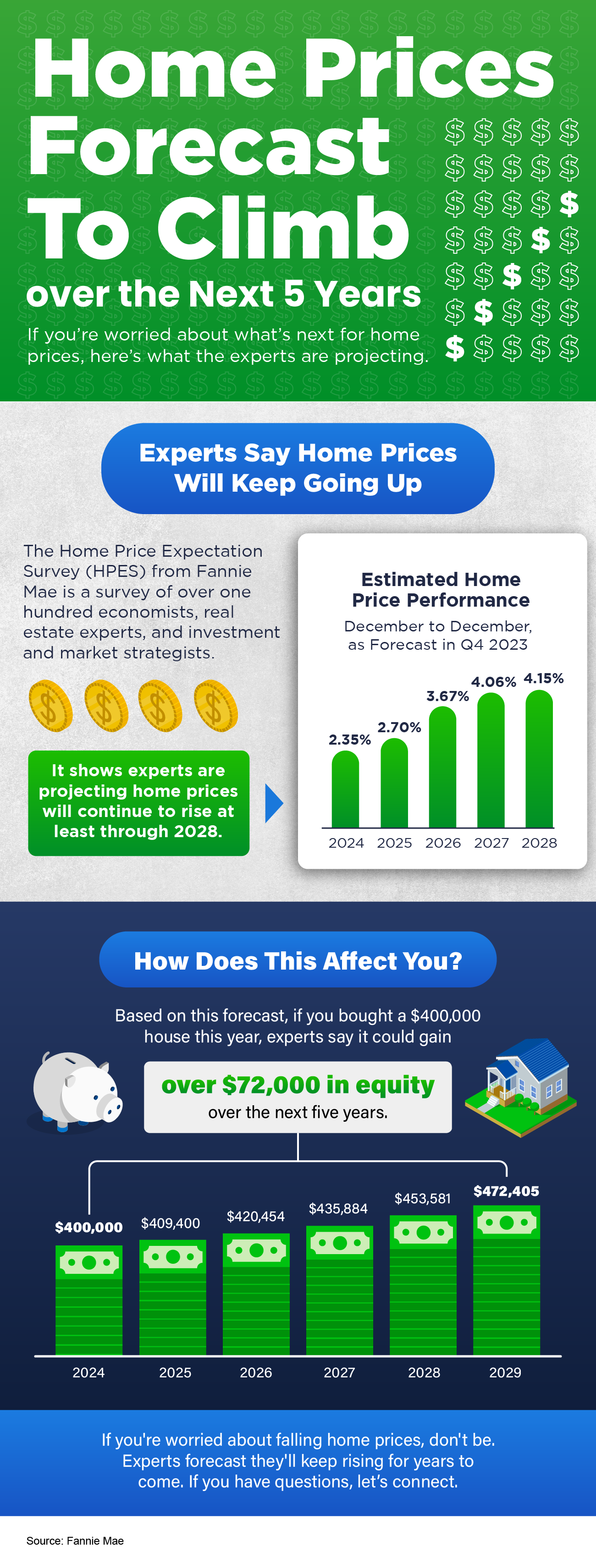

Home Prices Forecast To Climb over the Next 5 Years [INFOGRAPHIC]

Some Highlights

- If you’re worried about what’s next for home prices, know the HPES shows experts are projecting they’ll continue to rise at least through 2028.

- Based on that forecast, if you bought a $400,000 house this year, experts say it could gain over $72,000 in equity over the next five years.

- If you’re worried about falling home prices, don’t be. Many experts forecast they’ll keep rising for years to come. If you have questions, let’s connect.

Why the Price of Your House Matters When Selling

The asking price for your house can greatly affect your bottom line and how fast your house sells. Let’s connect so we can find the right price for your house.

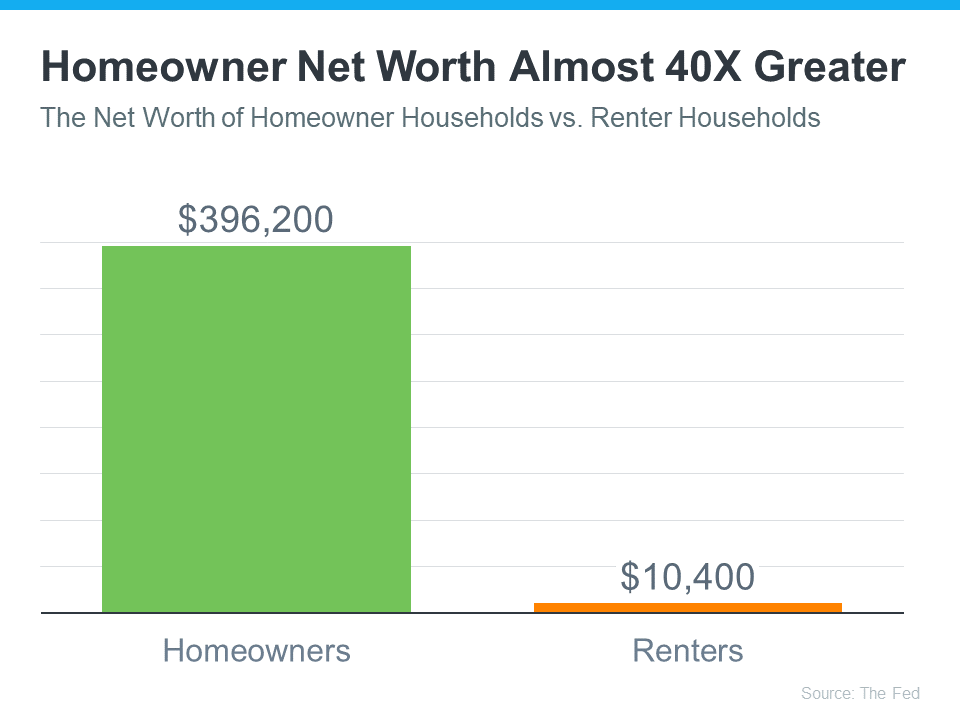

The Dramatic Impact of Homeownership on Net Worth

If you’re trying to decide whether to rent or buy a home this year, here’s a powerful insight that could give you the clarity and confidence you need to make your decision.

Every three years, the Federal Reserve releases the Survey of Consumer Finances (SCF), which compares net worth for homeowners and renters. The latest report shows the average homeowner’s net worth is almost 40X greater than a renter’s (see graph below):

One reason a wealth gap exists between renters and homeowners is because when you’re a homeowner, your equity grows as your home appreciates in value and you make your mortgage payment each month. When you own a home, your monthly mortgage payment acts like a form of forced savings, which eventually pays off when you decide to sell. As a renter, you’ll never see a financial return on the money you pay out in rent every month. Ksenia Potapov, Economist at First American, explains it like this:

“Renters don’t capture the wealth generated by house price appreciation, nor do they benefit from the equity gains generated by monthly mortgage payments . . .”

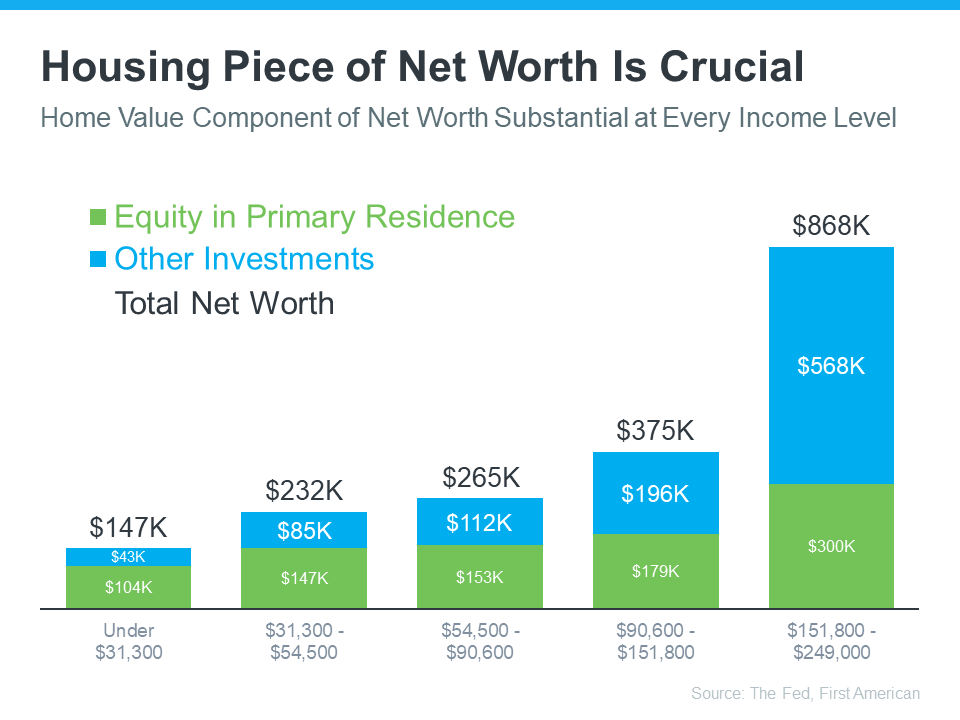

The Largest Part of Most Homeowner Net Worth Is Their Equity

Home equity does more to build the average household’s wealth than anything else. According to data from First American and the Federal Reserve, this holds true across different income levels (see graph below):

The green segment in each bar represents how much of a homeowner’s net worth comes from their home equity. Based on this data, it’s clear no matter what your income level is, owning a home can really boost your wealth. Nicole Bachaud, Senior Economist at Zillow, shares:

“The biggest asset most people are ever going to own is a home. Homeownership is really that financial key that helps unlock stability and wealth preservation across generations.”

If you’re ready to start building your net worth, the current real estate market offers several opportunities you should consider. For example, with mortgage rates trending lower lately, your purchasing power may be higher now than it has been in months. And, with more inventory coming to the market, there are more options for you to consider. A local real estate agent can walk you through the opportunities you have today and guide you through the process of finding your ideal home.

Bottom Line

If you’re unsure about whether to rent or buy a home, keep in mind that owning a home can increase your overall wealth in the long run, no matter your income. To discover more about this and the many other benefits of homeownership, let’s connect.